Ghana’s Smartphone Market in Flux: Samsung Surges as Tecno Slips (June 2024 – June 2025)

Setting the Scene: June 2024

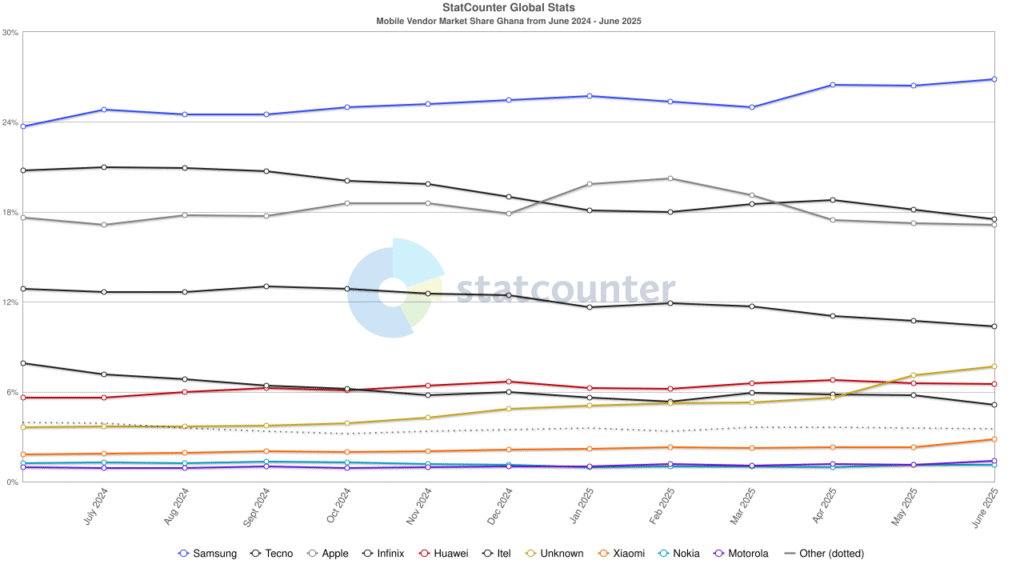

On a humid June morning in 2024, Accra’s Circle phone market felt as predictable as sunrise. Samsung banners draped the main thoroughfare, reflecting the brand’s comfortable 23 percent grip on Ghana’s smartphone landscape. Not far behind, Tecno’s blue‑and‑white kiosks pulsed with Afrobeats, their 21 percent share buoyed by the promise of big screens at modest prices. Apple, glassy and aloof, claimed roughly 18 percent, its devotees unfazed by premium tags. Beyond these marquee players, Infinix and Itel canvassed the budget quarter, luring first‑time buyers with loud FM radios and oversized batteries, while Huawei and Xiaomi remained fringe curiosities whispered about by tech bloggers. In side alleys, anonymous “GH₵400‑phones” changed hands in shoebox deals, but their presence barely registered on official charts.

So let’s dig into Statcounter’s latest data and see how the tug‑of‑war for smartphone dominance in Ghana has shifted over the past twelve months.

| Brand | June 2024 | June 2025 | Change |

|---|---|---|---|

| Samsung | 23.68 % | 26.83 % | 🔼+3.15 pts |

| Tecno | 20.75 % | 17.51 % | 🔽–3.24 pts |

| Apple | 17.61 % | 17.12 % | 🔽–0.49 pts |

| Infinix | 12.85 % | 10.37 % | 🔽–2.48 pts |

| Huawei | 5.60 % | 6.51 % | 🔼+0.91 pts |

| Itel | 7.92 % | 5.10 % | 🔽–2.82 pts |

| Unknown | 3.64 % | 7.71 % | 🔼+4.07 pts |

| Xiaomi | 1.84 % | 2.83 % | 🔼+0.99 pts |

Samsung is Closing in on 30 Percent of Ghana’s Smartphone Market

Samsung is more than leading the pack; it is pulling away. In twelve months the brand’s active share in Ghana rose from 23.7 percent to 26.8 percent, putting the company within sight of the 30 percent mark that analysts call “dominant territory.”

Three forces explain the surge. First, Samsung flooded the mid‑range with Galaxy A‑series models that offer bright OLED screens, solid cameras, and three years of Android updates. Second, it bundled those phones with free Galaxy Buds, discounted data plans, and buy‑now‑pay‑later deals through MTN and Vodafone, making a GH₵2,500 handset feel almost as affordable as a GH₵1,500 one. Third, the company spent heavily on visibility: billboards across Accra and Kumasi promised “5G for Everyone,” while weekly social‑media giveaways kept Galaxy devices in the conversation.

If this momentum holds, Samsung may cross the 30 percent threshold within the next year, a level of market control few rivals have ever reached in Ghana’s crowded smartphone arena.

Tecno’s Sudden Slide

Tecno began last year as Samsung’s nearest challenger. Its blue‑and‑white booths were everywhere, and the brand’s catchy jingles promised big screens at bargain prices. Yet by June 2025 Tecno’s share had fallen to 17.5 percent, a full three points below where it stood twelve months earlier. The slip was gradual but steady, and shoppers offered a simple explanation: nothing felt new.

While Samsung dazzled buyers with financing plans and camera upgrades, Tecno refreshed its Spark and Camon lines with only minor tweaks. Word spread quickly that the latest models looked and performed much like the phones from the year before. At the same time, no‑name imports undercut Tecno on price, and Xiaomi began offering brighter displays and larger batteries for only a little more money.

Marketing could not bridge the gap. Billboard slogans and music‑video tie‑ins kept Tecno visible, but visibility is not the same as excitement. By the time the June numbers were tallied, many long‑time Tecno users had either traded up to Samsung or switched down to cheaper unbranded phones. The brand now faces a clear choice: introduce hardware that truly surprises buyers or risk losing even more ground in the year ahead.

Infinix and Itel Lose Their Edge

Tecno was not the only Transsion brand feeling the squeeze. Its siblings Infinix and Itel also watched their foothold erode during the same twelve‑month stretch. Infinix slipped from 12.9 percent to 10.4 percent of active devices, while Itel dropped from 7.9 percent to 5.1 percent.

Two problems drove the decline. First, Samsung’s financing plans attracted many aspirational buyers who might once have settled for a mid‑tier Infinix model. Second, an influx of ultra‑cheap imports lured budget shoppers away from Itel’s entry‑level lineup. That left both brands squeezed in the middle, offering prices that were no longer the lowest and features that were no longer unique.

Retailers reported a common pattern: when customers compared an Itel handset with an unbranded import, they often chose the no‑name device once they saw the same battery rating at a lower price. For Transsion the message is clear. Incremental camera upgrades and minor design tweaks will not win back value‑driven buyers. The company must introduce genuine innovations such as faster charging or standout software perks before more shoppers migrate to the anonymous phones now crowding Ghana’s stalls.

The Quiet Surge of No‑Name Phones

While Samsung moved up and Tecno slipped, an unexpected group raced forward: phones with no recognizable brand at all. Statcounter lists them under “Unknown,” but to shoppers they are the GH₵400 to GH₵600 handsets offered in suitcases and small roadside stalls. Over the past year these models doubled their footprint, climbing from 3.6 percent to 7.7 percent of the market.

Their appeal is straightforward. A typical unbranded phone promises a large display, dual‑SIM support, a massive 6,000 mAh battery, and fast charging features that once cost far more. For parents buying a first device for a secondary school student, or for traders who need a tough backup handset, brand prestige matters less than price and battery life. Sellers in Kumasi, Tamale, and Cape Coast report that these devices move quickly, especially when the cedi weakens and household budgets tighten.

How the Other Players Carved Their Own Paths

- Apple slipped only slightly, easing from 17.61 percent in June 2024 to 17.12 percent in June 2025, showing that iPhone devotees remain loyal even when prices stay high.

- Huawei climbed from 5.60 percent to 6.51 percent by pitching Y‑series phones as long‑battery, mid‑range bargains.

- Xiaomi nearly doubled its share, leaping from 1.84 percent to 2.83 percent on the back of Redmi Note flash sales and campus buzz.

- Motorola inched up from 0.94 percent to 1.41 percent, winning commuters who want clean Android and all‑day Moto G stamina.

- Oppo crept from 0.57 percent to 0.84 percent with Reno and A‑series devices that mix flashy colours with super‑fast charging.

- Google Pixel edged from 0.43 percent to 0.58 percent, its grey‑market imports tempting camera purists who insist on stock Android.

- Nokia slipped from 1.22 percent to 1.10 percent; rugged builds and Android One updates kept loyal fans, but dated styling slowed new sales.

What the Shifts Mean for 2026

If Samsung keeps combining affordable Galaxy A models, two‑year financing plans, and constant 5G advertising, it could pass the thirty percent mark and secure a lead that will be hard to challenge. Tecno now stands at a crossroads: without a clear jump in hardware such as better cameras, faster charging, or a bold price reset, its three‑point drop may continue.

At the budget end, no‑name imports are still gaining momentum. Unless well‑known low‑cost brands slash prices, phones selling for under six hundred cedis may soon reach double‑digit share. Xiaomi and Huawei have quietly become the ones to watch. Their steady gains hint that each could overtake Infinix in the mid‑range tier before year‑end, especially if campus buzz and online flash sales persist. Apple is likely to hold its premium niche stable but unlikely to grow unless economic conditions improve and put new iPhones within easier reach.

All signs point to a fierce mid‑range battle in 2026. Features once reserved for flagships, such as 120 hertz screens, sixty‑five‑watt charging, and AI‑enhanced cameras, are moving into phones that cost between two and three thousand cedis. Consumers should see more value than ever, while manufacturers will face even tougher pressure to innovate and compete on price.